Despite bold declarations from the Tinubu administration that Nigeria has “cleared” its debts to the International Monetary Fund (IMF), fresh data from the global lender tells a different story—one steeped in nuance, exchange rate losses, and persistent financial obligations.

According to the IMF’s latest financial update released on April 30, 2025, Nigeria still owes the institution a total of SDR125.99 million, which translates to approximately N274.66 billion using the prevailing exchange rate of N2,180 per Special Drawing Right (SDR), based on data from currency platform XE.

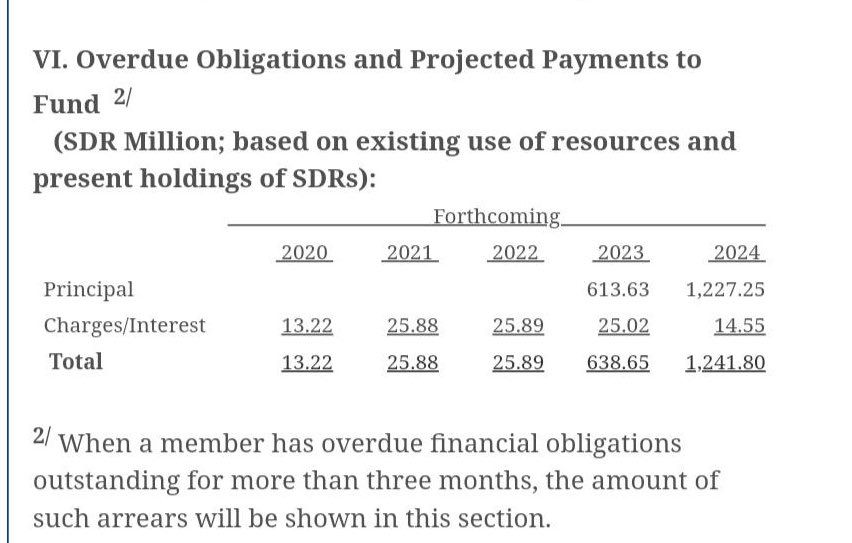

Breaking Down the Debt

The IMF debt Nigeria currently holds stems from a 2020 emergency loan of SDR2.454 billion, secured during the COVID-19 pandemic under the Rapid Financing Instrument (RFI) window. The debt includes both principal repayments and ongoing charges/interest, which must be paid over several years.

While Nigeria has reportedly met its principal repayment obligations—starting with SDR613.63 million in 2023, SDR1.227 billion in 2024, and another SDR613.63 million scheduled for 2025—the charges and interest continue to accumulate.

Here’s a snapshot of the projected annual payments in charges and interest:

2025: SDR22.35 million

2026 & 2027: SDR25.91 million (each year)

2028: SDR25.92 million

2029: SDR25.90 million

These obligations add up to SDR125.99 million, the amount Nigeria is still expected to pay, according to IMF records.

The FX Burden: Debt Doubled in Naira Terms

Even more striking is how Nigeria’s weakening currency has magnified its debt load. Data from the Central Bank of Nigeria (CBN), obtained by SaharaReporters, reveals that the country’s IMF obligations soared from N2.5 trillion in 2023 to a staggering N5 trillion by December 2024—a 100% spike due to naira depreciation.

In practical terms, while the dollar (or SDR) value of the debt hasn’t changed significantly, the Nigerian government now has to cough up twice the naira equivalent to meet its international commitments.

This forex-induced pressure has intensified concerns about Nigeria’s fiscal sustainability, as debt servicing continues to choke public expenditure. In January 2025 alone, Nigeria reportedly spent N696 billion servicing its debts—matching the figure for December 2024. The combined N1.3 trillion in just two months exceeded the monthly budgeted projection of N689 billion for debt servicing.

Most alarmingly, no capital expenditure was recorded in January 2025, according to the CBN’s economic report—a revelation that underscores how debt obligations are cannibalizing funds meant for national development.

In response to growing public concern, presidential aides Bayo Onanuga and Dada Olusegun have publicly dismissed reports that Nigeria still owes the IMF, insisting the debt has been fully repaid. However, both SaharaReporters and the IMF’s own database counter these claims, highlighting that while principal payments may have been fulfilled, interest and charges remain due and listed under “outstanding obligations.”

The data, in essence, paints a far more complex and burdensome picture than the narrative offered by government officials.

Conclusion: A Crisis of Perception and Policy

While it may be technically accurate that Nigeria is up to date on its principal repayments, the N274 billion in outstanding charges and interest, coupled with the devastating impact of forex losses, tells a deeper, more troubling story. The government’s insistence on claiming full debt clearance appears to be more political posturing than fiscal truth, especially when public spending continues to prioritize debt repayment over capital development.

As Nigeria grapples with the dual challenges of a depreciating currency and mounting fiscal pressure, the question remains: Can the Tinubu administration maintain this balancing act without sinking deeper into economic quagmire—or public distrust?